Key Findings on Social Security Reform

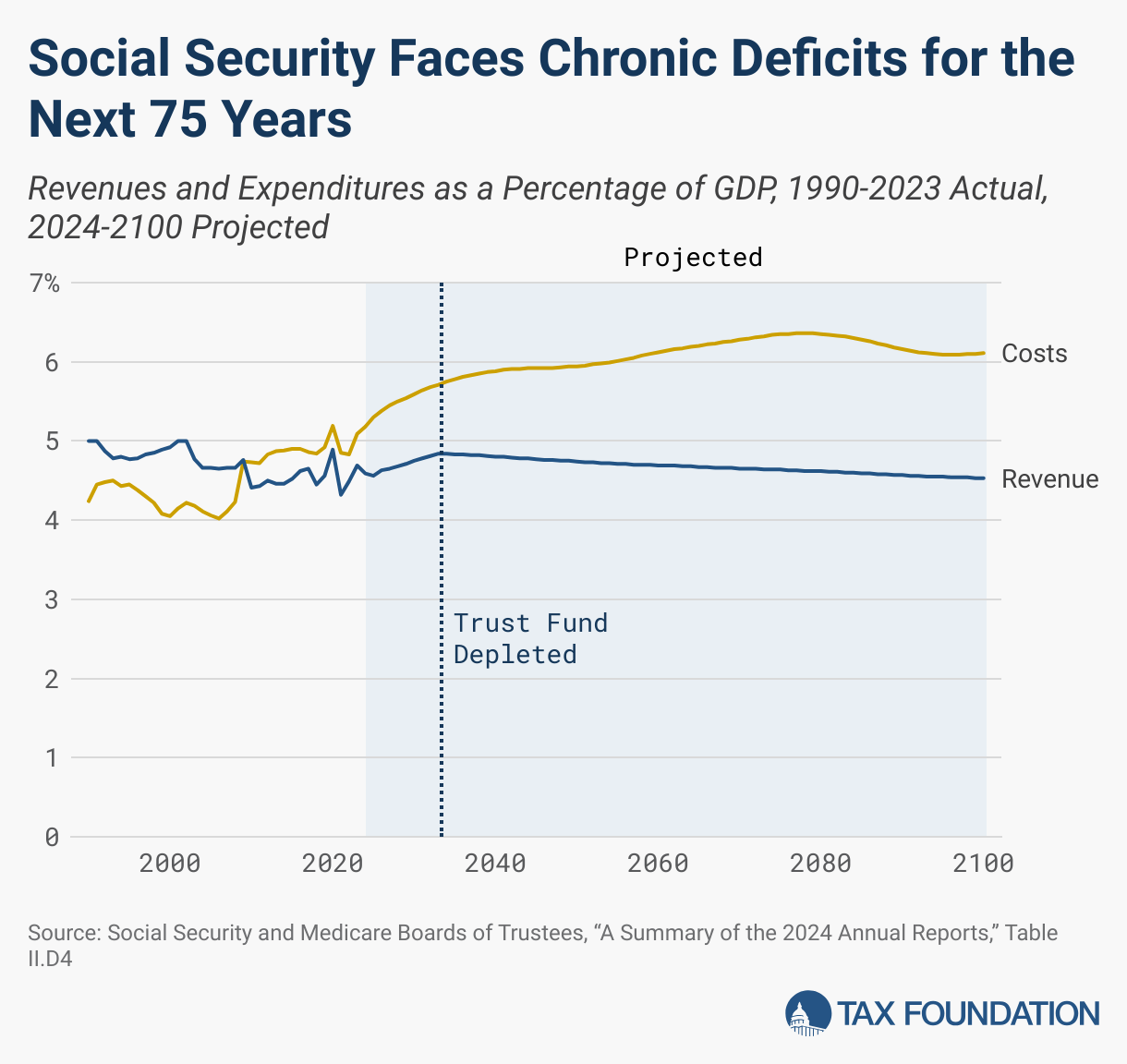

- By 2035, the Old-Age, Survivors, and Disability Insurance Trust Fund, or the Social Security Trust Fund, will be depleted, and current payroll taxes will only be able to fund 83 percent of the scheduled benefits.

- Absent any reforms, Social Security recipients would immediately face a 17 percent cut in benefits.

- Past reform efforts, such as the 1983 amendments, have not been able to solve Social Security’s long-term funding problem, which is due to a declining worker-per-retiree ratio that now stands at only 3-to-1 and is projected to fall further.

- Reforms such as using price indexing instead of wage indexing to calculate benefits, raising the retirement age, using the chained CPI to adjust benefits for inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers fewer goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power., and raising the payroll taxA payroll tax is a tax paid on the wages and salaries of employees to finance social insurance programs like Social Security, Medicare, and unemployment insurance. Payroll taxes are social insurance taxes that comprise 24.8 percent of combined federal, state, and local government revenue, the second largest source of that combined tax revenue. cap would restore solvency to the system.

- The current Social Security system crowds out private saving and harms young workers and new entrants to the labor force.

- Policymakers should look to other countries for inspiration, including Chile, Singapore, Australia, and Chile, which have all reformed their systems to encourage personal saving.

Introduction to Social Security Reform

Social Security is the largest federal government spending program, constituting 21 percent of the budget, or $1.3 trillion, in FY 2023—larger than the entire nondefense discretionary budget. The latest trustees report shows the program is on a fiscally unsustainable path that will exacerbate the US debt crisis if its imbalances are not addressed in the near term. By 2035, the Old-Age, Survivors, and Disability Insurance (OASDI) Trust Fund will be depleted, and current payroll taxes will only be able to fund 83 percent of the scheduled Social Security benefits. Absent any reforms, Social Security recipients would immediately face a 17 percent cut in benefits.

As it stands, neither major party candidate seeking the presidency of the United States has indicated that they would significantly alter the program’s negative trajectory, and one proposal would actually worsen it. Former President Donald Trump has indicated that he would prohibit any benefit cuts and consider exempting Social Security benefits from taxation, accelerating insolvency by six years. Vice President Kamala Harris has not yet made any formal statements on how she would alter the program, but her voting record in the Senate suggests she would be open to raising payroll taxes on high earners, which alone is not sufficient to close the funding gap.

Fortunately, we can draw lessons from past reform efforts to stave off the coming crisis. Reforms will involve politically difficult choices, but they are necessary to ensure a broad-based and universally accessible retirement system exists for future generations and is not threatened by funding cliffs. We can also look to other countries that have faced similar crises to learn how they reformed their retirement systems over time. This article will consider comprehensive reforms in Sweden, Australia, Singapore, and Chile; while none of their systems are perfect, they demonstrate the feasibility of significant improvements to how the federal government incentivizes saving for retirement.

How Social Security Works

Social Security is a defined benefit pension system, where benefits are calculated based on a predetermined formula that accounts for a retiree’s earnings over time. Under this system, current payroll taxes fund current retirees, resulting in a “pay-as-you-go” system. The pay-as-you-go structure means the fiscal health of the program depends on how many workers contribute through payroll taxes each year.

Social Security payroll taxes are applied to an earner’s wage income, up to $168,600 for 2024. The current Social Security payroll taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. rate is 12.4 percent, split between the employer and employee.

Social Security benefits are calculated based on the average wage-indexed monthly earnings over a retiree’s career. The formula replaces a larger share of income for lower earners relative to higher earners, and the relative replacement rates will remain constant over time no matter how high wages grow, since the benefits themselves are indexed to real wage growth. Although the program is not explicitly means-tested, in the sense that all retirees receive some benefit regardless of how high their incomes were during their working years or how many assets they currently hold, the formula ensures that the program is progressive.

The tax treatment of benefits also contributes to the system’s progressivity. Joint filers with less than $32,000 of income, and single filers with less than $25,000, face no tax on benefits (income is defined as “modified adjusted gross incomeFor individuals, gross income is the total pre-tax earnings from wages, tips, investments, interest, and other forms of income and is also referred to as “gross pay.” For businesses, gross income is total revenue minus cost of goods sold and is also known as “gross profit” or “gross margin.”,” or adjusted gross income plus tax-exempt interest plus half of Social Security benefits). Households earning between those thresholds and $34,000 for single filers and $44,000 for joint filers face taxation on half of their benefits. Above those levels, up to 85 percent of benefits are taxable.

Recipients can receive full benefits starting at age 67 for people born in 1960 or later. They may start receiving partial benefits as early as age 62, subject to an early retirement penalty. A delayed retirement credit up to age 70 is also available.

Under the current three-bracket calculation system, higher earners receive a smaller share of their lifetime earnings compared to lower earners. For example, Social Security benefits will replace 90 percent of the first $1,174 in average indexed monthly earnings. But for the next $5,904 in monthly income, the replacement rate falls to 32 percent of earnings. For earnings in the third bracket, up to the maximum of $14,050 (equivalent to $168,600 in annual income), the rate falls further to 15 percent. Income earned in excess of the maximum is not replaced.

The dollar thresholds separating the brackets (which the actuaries call “bend points”) are adjusted each year to match the rise in average wages covered by Social Security in the economy. That results in a constant set of replacement rates over time for low-, average-, or upper-income retirees. Constant replacement rates do not mean constant benefits, but they do mean that as wages rise in real terms over time, the benefits will keep pace to maintain the existing ratios.

The trustees report assumes that real wages will grow in the long run by 1.14 percent annually, boosting real benefits accordingly at all income levels. For example, lower-income workers (with average earnings over a 35-year period of $31,100) will on average receive benefits of $18,000, for a replacement rate of 58 percent. By the end of the century, lower-income workers will receive real benefits 43 percent higher than benefits paid to current medium-wage workers. And medium-wage workers, who currently receive $29,800 in benefits, will receive real benefits 79 percent higher than benefits paid to current high-wage workers. Benefits are even higher for people qualifying for the 50 percent spousal benefit for married couples, or up to twice as much in cases where both spouses worked and qualified for benefits.

Why Social Security Is Facing a Crisis

In 1960, 20 years after Social Security issued its first payments, the ratio of workers to retirees stood at 5 to 1. It has since fallen to 3 to 1 and is expected to fall to 2 to 1 by 2030. Since the Great RecessionA recession is a significant and sustained decline in the economy. Typically, a recession lasts longer than six months, but recovery from a recession can take a few years., Social Security has been in a persistent deficit, as benefit payments have consistently exceeded payroll tax receipts. The OASDI Trust Fund has covered the gap, but by 2035, it will be depleted.

The program’s projected costs continue to balloon over the next 75 years due to increasing numbers of retirees, expanding longevity, and declining fertility. The latest trustees report shows that payroll taxes would have to rise by 3.5 percentage points, or 28 percent, to cover the shortfall.

The recurring deficits of the Social Security system are primarily the result of a clash between the falling ratio of workers to retirees and the wage-indexed benefit formula that seeks to keep replacement rates constant per retiree at every point in the income distribution. Another smaller factor is the falling share of earnings subject to payroll tax due to the rise of tax-exempt employer-sponsored health insurance and other fringe benefits, as these benefits are a much larger share of total compensation than they were decades ago. To truly bring the system into balance, either fertility rates must permanently increase sharply, tax rates or the tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. must increase, or the formula must allow the replacement rates to decline over time.

Substituting Real Personal Saving for Part of Our Tax and Transfer System

The current Social Security system in the United States relies heavily on the tax and transfer system rather than on personal saving. One reason the status quo remains popular is that a defined benefit system like Social Security eliminates some uncertainty involved when saving for retirement. Benefits are “guaranteed” by law to the recipient upon retirement, regardless of how the financial markets and the economy perform. And many workers will receive more than they paid into the system in nominal dollars. The average middle-income couple will have paid $783,000 in taxes and receive $831,000 in benefits. Low earners will receive even more generous benefits relative to what they paid in taxes because of the progressive benefit formula.

However, the system contains several drawbacks. First, it is not totally free from uncertainty. Economic downturns can cause payroll tax revenue to slow and projected Social Security deficits to increase, as happened in the early 1980s. Congress has been compelled in the past to reduce the benefit structure in such circumstances, as it was in 1983.

Second, while Social Security provides generous benefits for retirees with low incomes, and many workers can expect to receive more from Social Security than they paid into it, it is a raw deal for many workers compared to the savings they could accumulate if they had the option to invest in personal accounts. A worker’s contribution to Social Security through payroll taxes earns about a 3 percent real rate of return over the long run, whereas investors can expect a 7 percent real rate of return holding stocks.

Of course, there is no free lunch: the higher return in the stock market compensates savers for the higher risk. Nonetheless, private accounts would give taxpayers the choice of how much risk they are willing to bear as well as options to diversify their portfolios beyond low-yielding Treasuries. As an example, a young entrant into the workforce could invest heavily in equities and then shift to bonds and less risky assets as they age.

The government system thus contains several vulnerabilities. As funds are invested in low-yielding Treasuries, the financial health of such a system depends on the size of the working-age population and how much workers pay in payroll taxes. Unlike defined contribution systems, where taxpayers deposit funds into their own personal accounts, and are therefore self-funding, defined benefit systems will always risk being underfunded.

The other issue with the current Social Security system is that it limits the ability of young earners to save independently of the current system for their own retirement. Social Security crowds out private saving in two ways. First, it collects payroll taxes from the working-age population. Many of the workers subject to the payroll tax have just entered the labor force, earn lower wages than more experienced workers, and thus are not able to save as much as they would in the absence of a payroll tax.

Second, because households receive Social Security when they retire, they are less likely to save than they would if Social Security did not exist. Of course, some households also save less because they might be short-sighted, make bad investments, or have incomes so low that their ability to save is constrained.

Under the current system, the burden of the payroll tax and the knowledge of guaranteed benefits in the future reduces some saving, yet many households still save outside of Social Security. For individuals 65 and older, Social Security represents about 30 percent of their total income. Less than 15 percent of the retired population rely on Social Security for 90 percent or more of their income. Many individuals save independently, and more than half participate in a defined contribution or defined benefit pension plan through their employer.

The current system also has implications for intergenerational transfers. When individuals die in old age, they pass on their wealth to their children or close friends. But because Social Security “wealth” is not owned by them, they do not pass on any benefits that they would have if they had managed their own personal accounts. Currently, only about 1 in 5 households receive an inheritance according to the Federal Reserve Board’s Survey of Consumer Finances, but it is possible this would be higher under a different system of saving.

Learning from Past Reform Efforts

The last time Social Security was reformed was in 1983. During the early 1980s, the economy was battered by high inflation, high unemployment, and wage stagnation, resulting in lower payroll tax revenue than would be needed to fund benefits for retirees. The situation was even more dire than it is today; when the reforms were actually enacted, the OASDI trust fund was scheduled to run out that year. The bipartisan 1983 changes gradually raised the full retirement age from 65 to 67, raised the payroll tax by 1.6 percentage points, and introduced the taxation of benefits.

The reforms brought Social Security into a surplus for nearly three decades, until 2009, but did not solve the contradiction between the long-run demographic problem facing the program and the wage-indexed benefit formula. Even the 1984 trustees report projected a deficit over the next 75 years of 0.06 percent, with growing annual deficits in the later decades of the 75-year planning period. As early as 1993, the trustees were estimating the trust fund would be depleted by 2036.

Reforming Replacement Rates

Currently, the Social Security bend points (the income brackets used to calculate the replacement rates) are indexed to the average growth in wages. This originated in the 1977 Social Security amendments, which were designed to correct an earlier reform that overcorrected for inflation and jeopardized Social Security’s financing during the 1970s stagflation. The introduction of wage indexing, unfortunately, placed Social Security on a path of permanent instability.

In 1976, Congress convened a panel under Harvard Professor William C. Hsiao to correct the Social Security benefit formula that had led to skyrocketing replacement rates. The panel presented two options, each involving a benefit formula with bend points and fixed replacement rates. The first option indexed bend points to wage growth, while the second indexed them to price growth.

The Hsiao panel recognized that wage indexing would plunge Social Security into chronic deficits given the impending demographic changes—a finding consistent with an earlier report by retirement experts presented to the Senate Finance Committee in 1973. For this reason, the Hsiao panel recommended using price indexing, which would have reduced benefit growth over time, since consumer prices typically grow more slowly than wages. However, the Carter administration, organized labor, and the Social Security Administration itself preferred wage indexing; thus, the current system was born.

Converting to price indexing would be a huge step toward restoring permanent balance to Social Security. Had price indexing been implemented under Hsiao’s proposal, Social Security would have run surpluses every year from 1982 to 2023, except for 2021. There would have been temporary shortfalls starting in 2024, but by 2044, Social Security would have been running surpluses again. Surpluses in