Oregon Measure 118: The Hidden Sales Tax with Far-reaching Implications

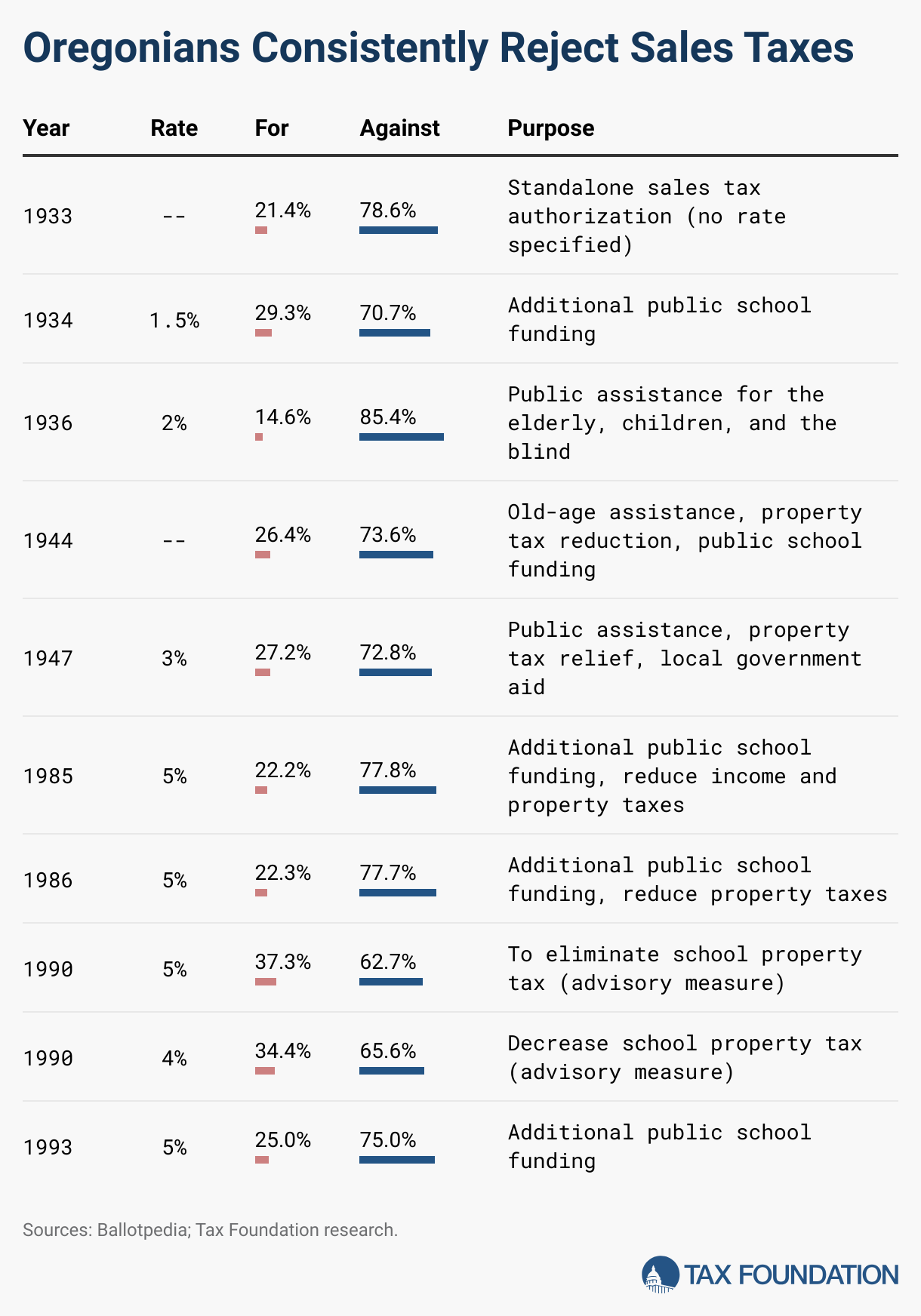

Oregonians have long stood united against sales taxes. Since a constitutional amendment in 1910 banned a sales tax, voters have rejected sales tax proposals 10 times. The only two occasions where opposition fell below 70 percent were advisory measures in 1990 regarding the elimination of school property taxes.

Today, Oregon faces a new tax proposal that could have even more dramatic effects: Measure 118. This measure, billed as a tax on large corporations, is essentially the most extreme sales tax yet. It applies multiple times on the same purchase, potentially leading to double-digit tax rates.

Measure 118 may appear as an attempt to target corporations, but in reality, it functions like a severe sales tax on consumers. When retail sales taxes are levied, consumers ultimately bear the cost. Measure 118 follows the same principle, burdening consumers with much of the incidence. Not all costs are passed on, but a significant portion is—enough to make Measure 118 a scarier prospect than the 10 sales tax proposals voters have previously rejected.

Understanding Measure 118

Measure 118 proposes a 3 percent tax on the gross revenue of large corporations. At first glance, this seems like a straightforward tax on big businesses. However, it effectively acts as an aggressive sales tax on consumers.

Corporations in Oregon pay income tax on their profits (net income). The state also imposes a minimum tax on corporations with minimal taxable income, which would be replaced under Measure 118 by a 3 percent gross receipts tax. This new tax would more often than not be higher than the current income tax.

For example, a company with $50 million in Oregon-apportioned gross income and $4 million in profits would currently owe $294,000 under existing income tax rates. Measure 118 would increase that to $1.5 million—making the effective tax rate on profits 37.5 percent.

The Hidden Cost to Consumers

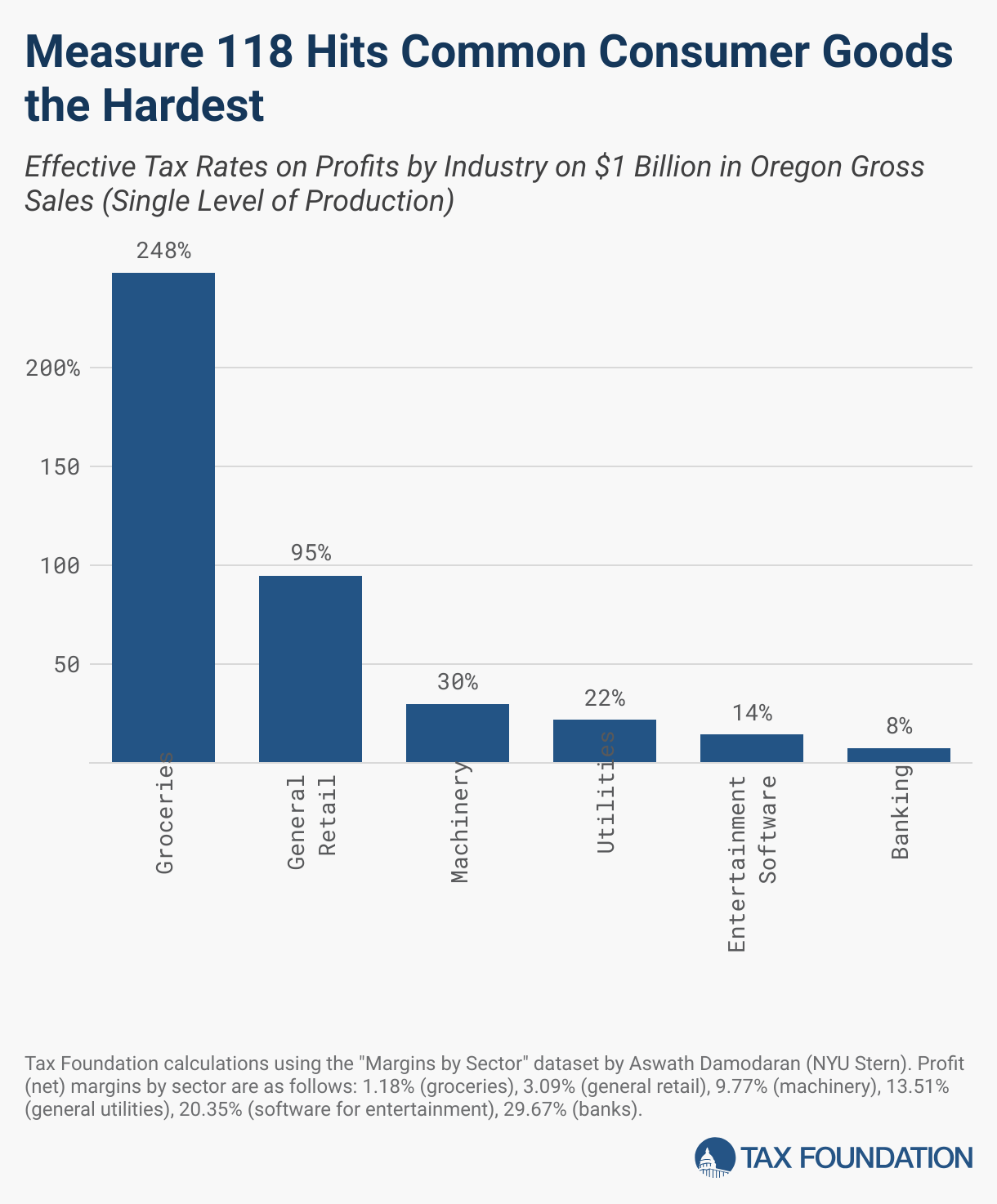

When a tax is imposed on the final sale, it operates much like a 3 percent sales tax on that transaction. Most large businesses (grocery stores, big box retailers, tech companies, etc.) will pass this cost on to consumers.

If the tax were solely at the retail level, it might be comparable to existing sales taxes in other states, which Oregon voters typically reject. However, Measure 118 also imposes the tax at the wholesale level and during various stages of the manufacturing process, embedding the tax at every stage of production.

This creates a cycle of tax pyramiding, where companies are taxed multiple times along the supply chain. In states like Washington, where gross receipts taxes are applied, the actual tax rate can be several times higher than the statutory rate due to tax pyramiding. In Oregon, pyramiding could result in consumer prices rising by an estimated 12 percent, effectively a 12 percent sales tax.

The Impact on Everyday Goods

To illustrate, consider a $10 frozen dinner. For it to reach consumers, a farmer grows the ingredients, which are processed into a meal, then transported to a grocery store. Every step involving a large business could be subject to the 3 percent tax, setting off a chain of tax pyramiding.

Starting with gross revenue, we calculate that the 3 percent gross receipts tax introduces an additional $1.09 to a $10 transaction—equivalent to a 10.9 percent sales tax. With pre-tax profits at just 5 percent, the tax amounts to 220 percent of pre-tax profits, forcing most of the cost to shift onto consumers.

Measure 118: A Bad Deal

Though intended to fund taxpayer rebate checks, Measure 118 essentially introduces a high and distortionary sales tax. Understanding this, the measure seems like a poor deal for both businesses and consumers.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Share