Latest Updates

- Note: We’ve adjusted our lower-bound revenue estimate for exempting all overtime compensation from income tax. Our new estimate accounts for the fact that BLS data only reflects the 50 percent premium on overtime compensation and not the base pay for overtime hours worked.

On Thursday evening, former President Donald Trump proposed a sweeping exemption from income taxA mandatory payment collected by governments to cover general services. for income earned from overtime work. This exemption would be added to Trump’s growing catalog of proposed tax cuts, including exemptions for tipped income and Social Security benefits.

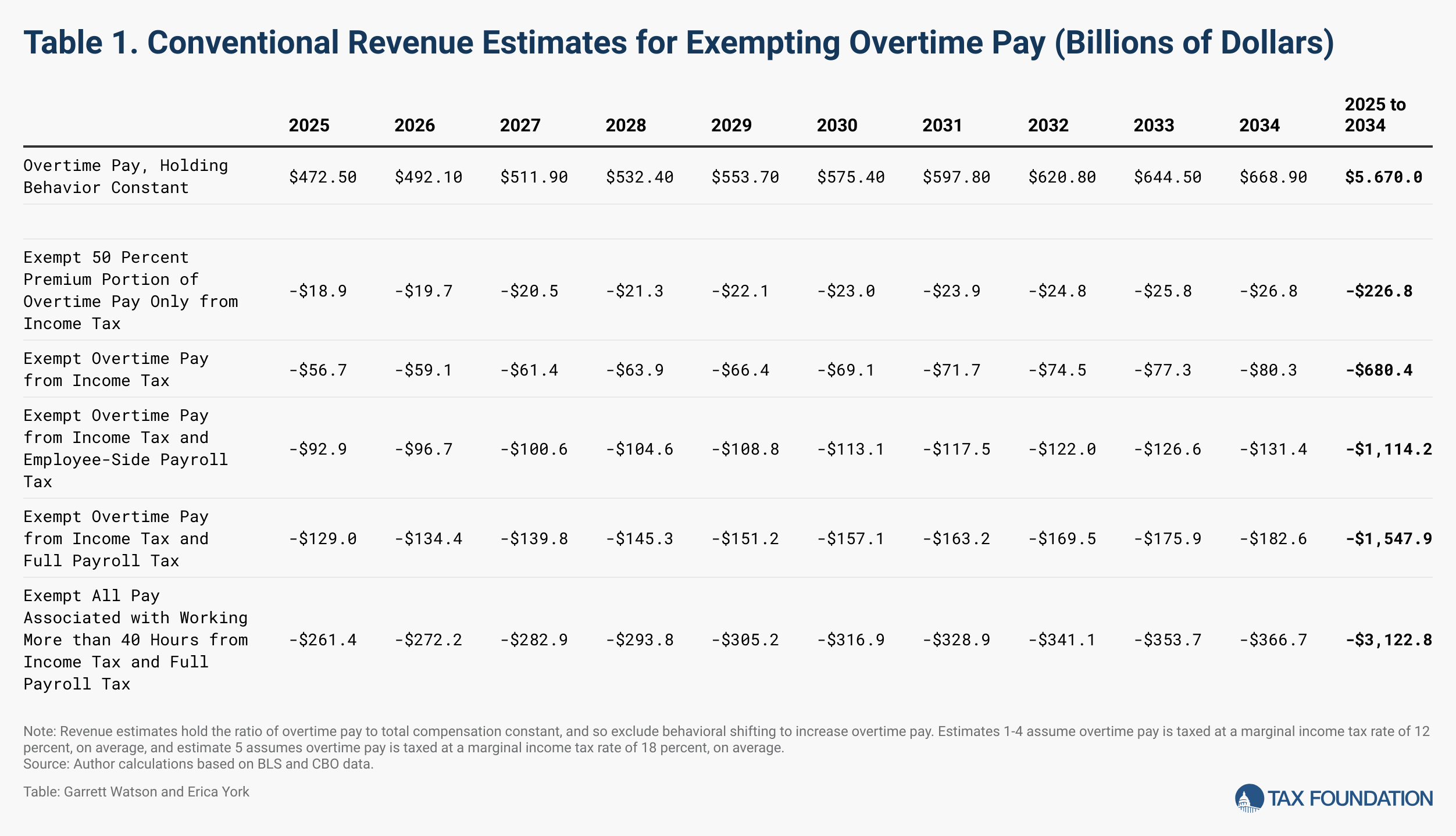

We estimate a lower-bound reduction in revenue for exempting all overtime pay from the individual income taxA tax on wages, salaries, investments, or other forms of income earned by individuals. to be $680.4 billion over 10 years on a conventional basis. This latest proposal would increase Trump’s total promised tax cuts from $6.1 trillion to $6.8 trillion, raising the deficit impact of his tax and tariffTaxes imposed on imported goods. plans to $2.0 trillion over 10 years.

If the proposal also exempts overtime pay from employee-side payroll taxes—6.2 percent for Social Security and 1.45 percent for Medicare—the combined impact would reduce tax revenues by $1.1 trillion over 10 years.

The uncertainty around the proposal’s specifics adds complexity to the revenue effect. If it exempts both income tax and both sides of the payroll taxA tax on wages and salaries to finance social insurance programs., the cost could exceed $1.5 trillion over 10 years. Conversely, a narrower proposal that exempts only the 50 percent overtime premium from income tax would reduce revenue by about $227 billion over 10 years.

Key details remain missing from the overtime proposal, and exempting it from income tax would significantly distort labor market decisions. Employees would favor overtime work, making hourly or non-exempt salaried jobs more attractive unless extended to exempt employees under Fair Labor Standards Act (FLSA) overtime rules.

For employers, Trump’s proposal would elevate labor costs due to increased overtime requests. Some businesses might find this fits their operations, while others would need to actively manage overtime to control costs.

Using Bureau of Labor Statistics data from 2023 showing 34.4 million workers working over 40 hours a week, we illustrate that exempting all income for such hours from income and both sides of payroll tax could have a fiscal cost of $3.1 trillion over 10 years (excluding interest costs).

{kind=link}

From a tax policy perspective, there is no principled reason to treat overtime income differently than regular income. For FLSA non-exempt and hourly employees, employers must pay 1.5 times the regular rate for overtime hours. Overtime pay is normally aggregated with other income for consistent tax treatment across all workers. Trump’s proposal, however, applies a “zero tax rate on a completely unprincipled definition of income,” as former Congressional Budget Office director Doug Holtz-Eakin remarked.

This new exemption would increase the focus on overtime decisions and tax arrangements, detracting from productive activities. Although it may slightly boost labor supply and long-term economic growth, simpler strategies like lowering statutory tax rates would achieve those goals without complicating the tax code further.

Compared to Trump’s other tax proposals for tips and Social Security, the overtime exemption is more complex. It requires a new tax code distinction based on hours worked, needing greater information reporting and administrative checks.

In summary, exempting overtime pay would overly complicate the tax code, increase compliance and administrative costs, and disrupt market neutrality by favoring certain work arrangements over others.

Revenue Estimating Notes

The Bureau of Labor Statistics estimates that overtime and premium pay constitute about 3.0 percent of total compensation, or 4.2 percent of salaries and wages. Holding this ratio constant over a decade totals approximately $5.7 trillion in overtime and premium pay. As this excludes recent rule changes by the Biden administration to expand overtime pay coverage, it assumes a reversal under a second Trump administration.

Similarly, maintaining a constant ratio of overtime pay excludes behavioral shifts to increase overtime hours worked or reclassify compensation. The strong incentive for such actions would be present.

We assume an average marginal income tax rate of 12 percent for overtime pay. For our upper-bound estimate, we use a marginal rate of 18 percent, based on current law rates, and assuming permanence of the 2017 tax law.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Share